On May 8, 2026, two announcements landed within hours of each other and told nearly opposite stories about the global battery storage industry. In Copenhagen, Danish utility Ørsted disclosed that it had purchased a 150 MW battery energy storage system in Michigan from developer ESA Solar Energy. In Oslo, Norwegian battery cell startup Morrow filed for bankruptcy. Both events were reported by Energy-Storage.News the same day.

Read together, they describe a market that is simultaneously consolidating at the project ownership layer and shedding industrial capacity at the cell manufacturing layer. That divergence is not coincidental. It captures the central thesis of where BESS investment currently makes — and does not make — economic sense.

Ørsted's Michigan acquisition

The transaction itself is straightforward. Ørsted, one of Europe's largest renewable energy developers and operators, acquired a 150 MW battery storage project from US-based developer ESA Solar Energy. Ørsted has not historically been a major BESS owner-operator outside its hybrid renewable portfolios, and the Michigan deal signals an evolving strategy for the company's US business.

Several aspects of the transaction reflect broader industry patterns:

- Operating asset versus development pipeline. Ørsted bought an asset, not a pipeline. The implied preference is for de-risked operating revenue over development-stage uncertainty.

- Geographic expansion outside core markets. Michigan is part of the MISO footprint, which has seen slower BESS deployment than ERCOT, CAISO, or the Northeast ISOs. Ørsted appears to be positioning early as MISO BESS market design matures.

- Portfolio diversification beyond offshore wind. Ørsted has restructured its global portfolio significantly over the past 24 months, including writedowns and divestitures in US offshore wind. Battery storage represents a different risk-return profile and a faster path to operating revenue.

The transaction terms were not disclosed publicly, but valuations for operating BESS assets in the US range broadly from US$300,000 to US$700,000 per MW depending on contract structure, market, and remaining warranty period.

Morrow's bankruptcy

Morrow Batteries — a Norwegian-headquartered cell manufacturer focused on stationary and industrial applications — filed for bankruptcy on the same day. The company had previously secured government and private funding to build domestic European battery manufacturing capacity, positioning itself within Europe's broader push for cell sovereignty.

Morrow's collapse is part of a broader pattern. European battery startups have struggled to compete with established Asian cell manufacturers (CATL, BYD, EVE, LG Energy Solution, Samsung SDI) on cost, scale, and time-to-market. Northvolt — the most prominent European cell hopeful — has faced repeated production delays and financial strain. Britishvolt collapsed in 2023. Morrow joins that lineage.

The structural reasons are well understood:

- Scale economics. Established Asian gigafactories operate at multi-GWh annual output with mature yields. New entrants face a steep ramp from pilot to gigafactory production.

- Cost gap. Per-kWh cell prices from Chinese manufacturers continue to compress; new European facilities cannot match that cost basis without subsidy support.

- Capital intensity. Battery cell manufacturing requires billions of dollars of capex before meaningful revenue, and the path to profitability typically extends well beyond five years.

- Specification fragmentation. Multiple chemistries (LFP, NMC, sodium-ion) and cell formats (prismatic, cylindrical, pouch) divide investment across competing standards.

European policymakers continue to support domestic battery manufacturing through the European Battery Alliance and instruments like Important Projects of Common European Interest (IPCEI). The Critical Raw Materials Act sets benchmarks for EU-internal extraction, processing, and recycling. But the headline reality of 2026 is that one more European cell hopeful did not make it.

The two speeds

The contrast between Ørsted and Morrow is the contrast between two different layers of the BESS value chain:

Newsletter World BESS - Home

| Value chain layer | Capital flow direction (2026) | Recent evidence |

|---|---|---|

| Project ownership and operations | Strong inflows; consolidation | Ørsted–ESA Solar Energy (Michigan, 150 MW); Royal Vopak acquiring Green Energy Storage (Netherlands, 200 MW / 800 MWh pipeline); Innergex commissioning San Andrés II (Chile, 42 MW / 210 MWh) |

| System integration and EPC | Order book expansion | Fluence reported US$5.6 billion order backlog with 147 GWh pipeline; SPML Infra secured INR 1,128 crore from NTPC for 250 MW / 1,000 MWh in India |

| Specialty chemistry / flow battery | Selective venture capital | CMBlu Energy closed €50 million Series C with Samsung Ventures participation |

| European cell manufacturing | Persistent stress; failures | Morrow bankruptcy (May 2026); historical pattern with Britishvolt and Northvolt struggles |

| Sodium-ion cell capacity (China) | Strong commercial validation | CATL–Beijing HyperStrong 60 GWh partnership announced April 2026 |

The economic logic behind the divergence is consistent across geographies. Capital is flowing to where revenue durability is improving — operating projects with multi-year contracts, integrated systems with substantial warranty backstops, and chemistries that have already crossed the commercial-validation threshold. Capital is exiting where structural cost disadvantage persists, particularly for European cell manufacturing competing against Asian incumbents.

What it means for project developers

Three implications for BESS developers and asset owners are worth noting:

Operating assets are increasingly liquid. Ørsted's Michigan acquisition is one of several signals that secondary-market BESS asset trading is becoming a real feature of the industry. Developers structuring projects with eventual sale to a long-term owner have a clearer path than they did two years ago.

Cell sovereignty premiums are mostly notional. Western policy frameworks — IRA Foreign Entity of Concern restrictions in the US, EU Battery Regulation due diligence in Europe — are real, but they have not yet translated into significant economic premiums for non-Chinese cells in commercial procurements. Morrow's failure underscores that subsidy support has not been sufficient to bridge the cost gap.

Integration and software, not cells, are where differentiation lives. Fluence's US$5.6 billion backlog is built on platform integration and software. Sungrow's grid-forming PCS demonstrating 19-second black start at its new field test base in May 2026 is another example. The competitive moat is moving downstream from cells.

What to watch

Three near-term events will reveal whether the pattern holds:

- Whether other distressed European cell makers can recapitalize or follow Morrow's path. Northvolt's restructuring trajectory remains the bellwether.

- Whether Ørsted is the first of several European utilities expanding US BESS portfolios. Strategic acquisitions by RWE, EDF, and Iberdrola of operating US storage assets would confirm the trend.

- Whether sodium-ion validation accelerates capital flows to non-Chinese chemistry alternatives. US-based Peak Energy's 5 GWh sodium-ion supply agreement with Jupiter Power is the test case for whether a Western sodium-ion ecosystem emerges in parallel to China's.

The week of May 5 to 9, 2026, will not show up in any single industry report as a turning point. But it captured, in compressed form, the shape of where BESS capital is moving — and where it is exiting.

Sources: Energy-Storage.News archive (May 2026), including coverage of Ørsted's acquisition of 150 MW Michigan BESS from ESA Solar Energy, Morrow bankruptcy filing, and Royal Vopak agreement to acquire majority of Green Energy Storage; ESS News, "Fluence reports $5.6 billion order backlog as battery pipeline swells"; Taiyang News, "Global Battery Storage News Snippets — May 8, 2026"; CATL and Beijing HyperStrong Technology corporate communications; Peak Energy press releases.

Related Posts

Capital and Casualties: Ørsted Buys, Morrow Files — A Week in BESS M&A

A single week in May 2026 captured the energy storage industry's two-speed reality: Ørsted bought a 150 MW BESS in Michigan, Vopak acquired a Dutch storage developer, R.Power locked Axpo to optimize 1,200 MWh in Poland — while Norway's Morrow filed for bankruptcy. Inside the simultaneous flows of capital and casualties.

Global BESS Market Outlook 2026: Capacity, Trends and Key Players

A data-driven look at the global battery energy storage market in 2026 — installed capacity, regional leaders, leading manufacturers and the trends shaping the next phase of growth.

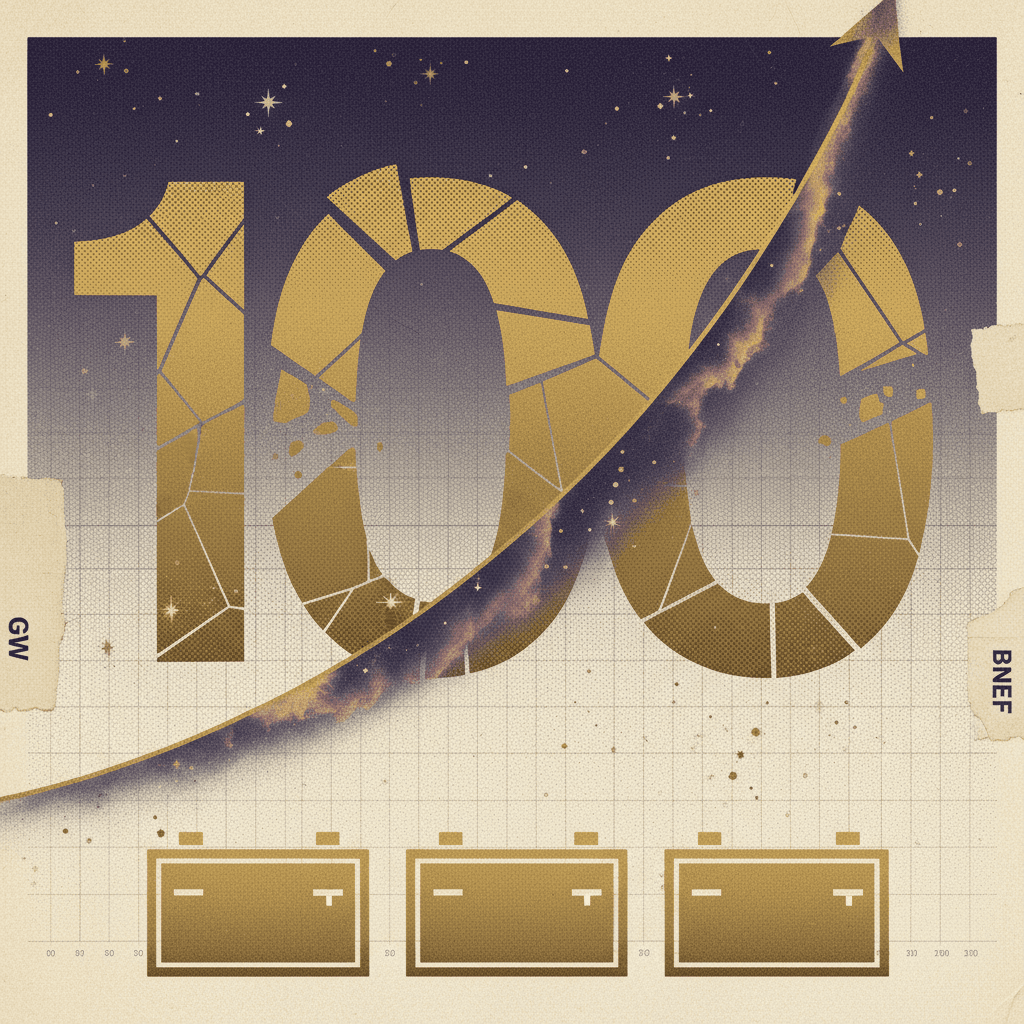

The 100-Gigawatt Era: BloombergNEF's 2026 Numbers on Storage's Scaling Curve

BloombergNEF reports global energy storage additions reached 112 GW in 2025 — up 48% year-over-year — and forecasts 158 GW for 2026. The data reframes how fast storage is scaling relative to solar and wind, and where the next wave of growth will come from.

BloombergNEF: Storage Hit 112 GW in 2025, Crossing the 100-Gigawatt Threshold

BloombergNEF reports global energy storage deployment hit 112 GW of annual additions in 2025 — crossing the 100-gigawatt threshold for the first time and forecasting 158 GW in 2026. Inside the numbers and what they mean for the rest of the decade.